Best Credit Card for Overseas Spending & No FX Fees

20 Mar 2026

With so many different credit cards out there – each with different perks, reward types, and fees – choosing the best one for overseas spending can be a mind-boggling task. How do you compare between cards when each of them have their own pros and cons?

Here’s a useful tip: As varied as they may be, most credit cards come with a foreign transaction fee. Most, but not all.

If you’re adamant about not paying extra fees when spending overseas, then you’ll want to exclude all those credit cards that come with a foreign transaction fee (there’re exceptions – we’ll get to those later).

That said, foreign transaction fees shouldn't be the only thing you consider before getting a credit card. You need to consider what's the annual fee, what rewards can you earn each month as well.

Clearly, there’s quite a bit to think about. Let’s zoom in for a closer look.

How To Avoid Foreign Transaction Fees?

If you want to avoid paying the foreign transaction fee, simply choose a credit card that comes with “no foreign transaction fee” or “zero FX fees.”

But first, let's discuss what exactly is a foreign transaction fee.

What is a foreign transaction fee?

Simply put, a credit card’s foreign transaction fee is an additional fee that is charged on transactions made in a currency other than SGD. This fee is automatically applied and added to your transaction, and you may not see it listed separately in your credit card statement.

This makes it difficult to see how much more you’re paying, which means you may be unaware of the impact on your overseas spending.

For the avoidance of doubt, credit card overseas transaction fees are typically made up of two parts:

(1) A fee paid to the payment network such as Mastercard or VISA (typically 1%), and;

(2) A currency conversion fee charged by the processing bank, which ranges from 2% to 2.25%.

What “no foreign transaction fee” really means

In the case of "No Foreign Transaction Fee", or commonly termed, "No FX Fees" - this means that you will not be charged the ~3.25% when you spend overseas or make a transaction in foreign currency online.

Whether it's for a last-minute getaway, or just shopping leisurely behind your computer, you can get away with this fee. And honestly, this gives anyone a peace of mind knowing that you will not be charged at all, except for your actual spends.

Find Out More About Mari Credit Card

Best credit card for overseas spending

Here’s a quick rundown of the cards known for not having any foreign transaction fees. Information is accurate as at the time of writing.

Source: Trust Bank, GXS Bank, UOB Bank

How to choose the right credit card with no overseas transaction fees (based on your travel profile)

Frequent travellers

If this sounds like you:

- You travel several times a year

- You actively redeem air miles

- You’re comfortable tracking credit card rewards

Tips on choosing the right credit card

Frequent travellers should focus less on foreign currency fees. Instead, pay attention to reward rates and perks – the value they provide can sometimes outweigh the foreign currency transaction fee. If that’s the case, it may be worth accepting the extra fee.

Casual travellers

If this sounds like you:

- You travel one to two times a year

- Your overseas spend is mainly on dining and shopping

- You prefer simplicity in your credit card rewards

Tips on choosing the right credit card

For casual travellers, it’s best to avoid paying the foreign currency transaction fee. There’s no point paying extra for your annual holiday after all. Look out for a card that gives you straightforward cashback with no hoops to jump through, and avoid complex rewards systems that require fulfilling several conditions.

Overseas online shoppers

If this sounds like you:

- You shop on overseas sites often

- Spend in foreign currencies without travelling

Tips on choosing the right credit card

For online overseas shoppers who don’t travel much, travel perks don't matter. Prioritise credit cards that provide rewards that apply to online transactions made in foreign currencies – this way you can enjoy more value from your online shopping.

Family travellers

If this sounds like you:

- Larger overseas expenses

- Multiple transactions per trip

Tips on choosing the right credit card

Family travellers are likely to spend larger amounts during overseas holidays, as they have to pay for multiple hotel rooms, plane tickets, meals, and other essential expenses. It’s important to avoid FX fees, which can add up to a significant amount during family trips. As you'll likely be spending on several different transactions, choosing a credit card that rewards a wide range of spending categories will be advantageous. Additionally, having easy spend tracking will allow convenient budget tracking throughout the trip.

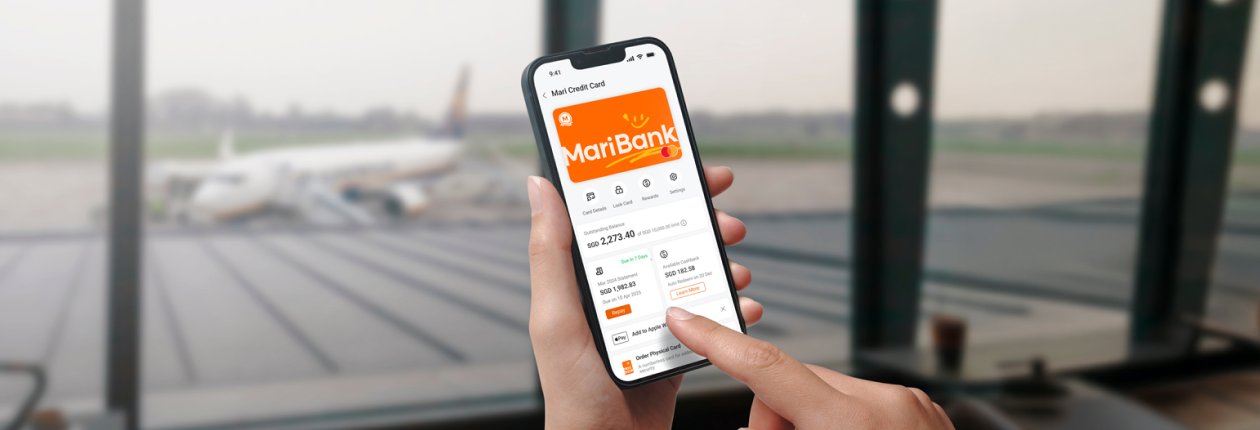

Mari Credit Card - Enjoy zero fees and 1.5% cashback on overseas spends

The Mari Credit Card is designed for those who want a simple and low-cost way to enjoy rewards when they spend overseas. What’s more, you’ll earn 1.5% cashback on eligible overseas spends – easy to do with worldwide Mastercard acceptance. One more thing to love about the Mari Credit Card, you can track your spending at a glance on the MariBank app, so you’ll always have control of your budget.

Apply For Mari Credit Card Now

Disclaimer

The contents in this webpage do not constitute the distribution of any information or the making of any offer or solicitation to anyone in any jurisdiction in which such distribution or offer is not authorized or to any person to whom it is unlawful to distribute such contents or make such an offer or solicitation.

The information provided here is intended for general circulation and/or discussion purposes only, and shall not be regarded as an offer, recommendation, solicitation or advice to buy or sell any product and shall not be transmitted, disclosed, copied or relied upon by any person for whatever purpose. Any description of products is qualified in its entirety by the terms and conditions of the product and if applicable, the prospectus or constituting document of the product. Nothing on this webpage constitutes accounting, legal, regulatory, tax, financial or other advice, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. If in doubt, you should consult your own professional advisers about issues discussed herein. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

Read More